Welcome to the 18th edition of our Weekly Musings!

The fall in 2020 started with the news of coronavirus induced pandemic and the subsequent lockdowns imposed by the government. The flagship indices, the Sensex and Nifty 50 declined by more than 35% in March and April 2020 as the benchmark Nifty suffered the worst ever March since its inception in 1994. Circa January 2021, the flagship indices hit their all-time highs of 47,980 and 14,049 respectively. A mammoth gain of close to 85% in just 3 quarters!

The GDP growth in the 2nd quarter of FY21 substantiates the performance of economic activities with a better-than-expected recovery in corporate earnings. High-frequency indicators such as railway freight volume, new property registrations (on the back of low-interest rates and indirect tax breaks), electricity consumption have formed a long-term growth trend thus reflecting a continuity in the betterment of India’s macro indicators.

Moreover, the steel demand in India is expected to rise more than 10 percent (as per industry estimates) in the next financial year against a lower base of FY21 due to the imposition of coronavirus induced lockdown in this year. This in turn will provide a much-needed boost for various participants of the economy as the stressed steel firms could witness higher volumes, subsequently higher operating margins, and thus will help their interest coverage to get better. With better interest coverage, banks and NBFCs also stand to benefit as the capital-intensive firms meet their interest obligations.

This situation is not only restricted to the steel sector but is spread out to other players in the infrastructure segment, such as the capital goods companies, cement, and other manufacturing companies.

FY 2021-22 could well be India’s year if the bottomed out corporate earnings and stressed capital-intensive businesses show some real strength and reduce their outstanding debt by taking advantage of overall lower interest rates.

Robust Auto Sales; Highest GST Collections – The Great Indian story goes beyond the narrative of pent-up demand

The automotive industry in India has been under tremendous pressure over the past couple of years. The industry, for two consecutive years, has been witnessing de-growth in terms of volumes. Several factors have been contributing to this decline including the transition from BS4 to BS6, the coronavirus pandemic, the rise of the gig economy, and a growing awareness of shared mobility.

All these factors together, significantly weakened the demand for automobiles, culminating in the worst ever performance posted by the auto industry. However, things seemed to have bounced back by the end of the year as the majority of vehicle manufacturers registered strong sales numbers for the month of December compared to last year.

For most listed original equipment manufacturers (OEMs), the wholesale (vehicles sold dealerships) volumes for the month of December came in better than expected despite lower discounts across all vehicle segments this time around. Factors such as low-interest rates, preference for personal mobility over public due to the pandemic, and improvement in consumer sentiment, contributed to the uptick.

In aggregate, the top six manufacturers sold 2,44,006 units in December 2020 in the domestic market compared to 2,04,169 units in December 2019, registering a 20 percent growth.

While several manufacturers credited the growth in sales to pent-up demand and festive sales, there is a perception that the demand going forward would be driven by vaccine and therefore, on the revival of the economy. The auto sales for the last 3 months of this financial year will be crucial to determine the future guidance of the auto industry as a whole.

The lockdowns induced by the pandemic in the first half of CY20 hit the auto sector hard as the need for mobility was constrained. However, the second half saw pent-up demand due to personal mobility needs and the rising optimism within the industry.

For CY21, a strong double-digit growth aided by the base effect can be foreseen. More importantly, the trends observed in the second half is likely to continue due to faster than expected recovery in economic activity and vaccination drive against coronavirus.

The biggest beneficiaries are likely to be affordable cars and two-wheeler makers as the preference for personal mobility gains momentum. Also, a rebound in infrastructure activity is expected to support the commercial vehicle segment.

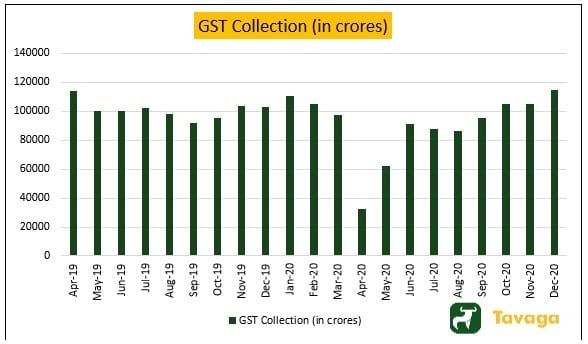

GST collections for the 3rd consecutive month remained elevated above the Rs 1 lakh crore threshold due to a pickup in consumption activities on the backdrop of improved macro-economic indicators, cheap credit, and pent-up demand.

Source: GST Portal, Tavaga Research

The revenue for November (collected in December) came in at Rs 1.15 lakh crore, the highest ever after the GST came into force. While this could well be an achievement, India has a long road ahead.

Factors that played a key role:

- Government’s tough stance against GST evasion and fake bills

- Stricter and tighter compliance measures

- An overall spike in demand + increase in consumption activities

- Pent-up demand

For the month of December 2020, the GST revenues from domestic transactions rose by 8 percent while that from imports grew by a healthy 27 percent signaling demand revival on high-end discretionary items such as cell phones, electronic items, and other white goods.

India’s fiscal deficit in the first 8 months of FY21 rises to 135% of the target

The Covid-19 pandemic has resulted in severe revenue stress for the government as India’s fiscal deficit soared to 135% of the budgeted estimates in the first half of FY21. With a sharp revenue shortfall, the total expenditure of the government has considerably risen than what was witnessed last year as the central government continues its spending activity to prevent the impact of the Covid-19 pandemic by way of a stimulus package.

While outlining the government’s resolve in supporting the economy post the initial detrimental effects of Covid-19, the finance minister had reaffirmed its willingness to continue spending activity on a large scale in order to infuse demand in the economy.

On a YoY basis, Capex grew by a whopping 248% in November 2020 compared to a growth of 130% in October 2020.

The difference between the government’s total revenue and expenditure stood at Rs 10.7 lakh crore between the start of FY21, i.e., between April and November. In the same period last financial year, the fiscal deficit was at 114.8% of the budget estimates.

The budget estimates and the subsequent targets are fixed in the month of February (every year) and could undergo a sharp revision due to the unanticipated effects of the pandemic. With the government staying firm to its enhanced gross market borrowing of Rs 12 lakh crore for FY21 and with no successful divestment yet, the fiscal deficit is expected to exceed 8% of the GDP against the initial expectations of 4%. Moreover, the much-awaited LIC IPO could also spill over to the next FY as various news reports indicated the same.

A rise in collections in the last quarter of 2020-21 due to a pick-up in the overall economy will be a major factor while revising the deficit projections for FY21. As the financial year closes in the next 3 months, the ambitious disinvestment targets of the government will be a thing to watch out for as various labor unions have already expressed displeasure over disinvestment, and this could well gather steam in the coming months like the ongoing farm protests.

Eventually, disinvestments could be delayed by a few more months, thus missing the target for FY21.

Coming Up In The Week:

- India December Manufacturing PMI – 4th January

- India December Import-Export Data – 4th January

- Meeting of OPEC nations – 4th January

- India December Services PMI – 5th January

- Corporate Earnings Season begins – 8th January

- US Unemployment Data – 8th January

Happy Investing!

Download the Tavaga Mobile Application And Link Your Trade Smart Trading Account: