Welcome to the 2nd edition of our weekly musings!

In the weekly musings published last week, we discussed the green shoots visible in auto sales, global trends in the oil market, and the soaring tension between states and center on GST revenue compensation. While the number of COVID-19 cases continues to surge in India, most economic metrics exhibit an improvement in their performance as the cities open all commercial activities.

Most states witnessed higher electricity consumption in the past week compared to a similar period in FY20. FASTag transactions continue to increase at a steady rate with an uptick in vehicular traffic. E-waybills generated in the first week of September, was higher than the daily average of August 2020. However, the consumption of petroleum products indicated a mixed outlook for the economy. While the consumption of petrol for the month of August was better than the previous months, the diesel consumption decreased by about 12% in August as compared to the figures reported in July. (Source: Ministry of Petroleum and Natural Gas)

India’s Industrial Output continues to Contract; slower Pace of Contraction a hope for the Industry:

India’s industrial production shrunk by 10.4 percent in July as per the data published by the Ministry of Statistics on 11th September. This was the fifth consecutive month of contraction, however, the rate of contraction was slower than June’s 15.7 percent.

Manufacturing output, which accounts for 78% of the index of industrial production fell 11.1% compared to a decline of 16% in June. Mining saw output fall by 13% in July, less than June’s 19.6 percent. Electricity generation continued to see a lower fall at 2.5 percent from the 10 percent decline in June.

The manufacture of tobacco products and pharmaceuticals saw a growth of 22% and 6.1% respectively. The rest of all the sectors continued to contract with auto, paper, and beverage sectors declining by more than 30%.

Except for consumer non-durables, whose output grew by 6.7% month on month, all the other categories of the industrial goods continued to witness a decline.

- Primary goods output growth contracted 10.9% in July, compared to a fall of 14.5% in June

- Consumer durables output fell 23.6%, compared to a fall of 34.25% in June

- Capital goods output fell 22.8% from a decline of 37.4% last month.

Rating Agencies cut India’s FY21 GDP estimates

After the Q1 GDP figures for FY21, almost all rating agencies further projected a steeper decline of India’s real gross domestic product. While cutting the forecast after the announcement of Q1 data, Moody’s stated that India’s policymakers have struggled to contain and mitigate the risks to India’s economy arising out of the pandemic.

It further added that it expects the central government to run a fiscal deficit of 7.5 percent which will eventually drive a higher debt burden on the country. As COVID-19 cases continue to soar in India, the agency also warned about the return of lockdown measures which can be detrimental to India’s economic recovery.

GDP Contraction Projection

| Rating Agency | Before Q1 GDP figures (in %) | After Q1 GDP figures (in %) |

| Goldman Sachs | 11.10 | 14.80 |

| India Ratings | 5.30 | 11.80 |

| SBI Research | 6.80 | 10.90 |

| Nomura | 6.10 | 10.80 |

| Fitch | 5.00 | 10.50 |

| ICRA | 9.50 | 9.50 |

| Crisil | 5.00 | 9.00 |

| Moody’s | 4.00 | 11.50 |

| Care Ratings | 6.40 | 8.00-8.20 |

Source: Business Standard, Tavaga Research

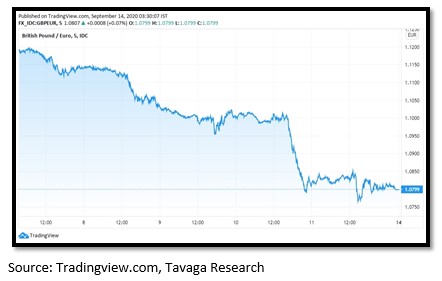

Pound falls as Brexit Stalemate Continues:

With tensions rising between the United Kingdom and the European Union over the Brexit deal, the pound settled near 6-month lows against the Euro.

5-Day Performance of British Pound against EURO

On Thursday, with a drop of more than 1.5%, the Sterling witnessed its biggest daily fall since March as the EU threatened to take legal action against the UK as the latter plans to break the international law in a very specific and limited way.

Coming Up in the Week:

- 14th September: August CPI and WPI inflation

- 15th September: India’s Trade Deficit for August

- 16th September: Fed Rate Decision

Happy Investing!

Tavaga Advisory Services is the official partner for providing advisory services to TradeSmart clients

Tavaga & Trade Smart has issued this report for information purposes only. This is not an investment document.

Please refer to https://tavaga.com/terms.html for disclosures.