What Are Futures?

Feb 16 2022 7 Min Read

A future is an important derivative trading financial instrument. Before we dive deep into the subject it is essential for us to know what a derivative trading instrument is.

What is a derivative?

A derivative, as the name suggests, is a product whose value is derived from one or more underlying variables. The underlying variables can be either stock, foreign currency or even interest rates like LIBOR, OIS etc.

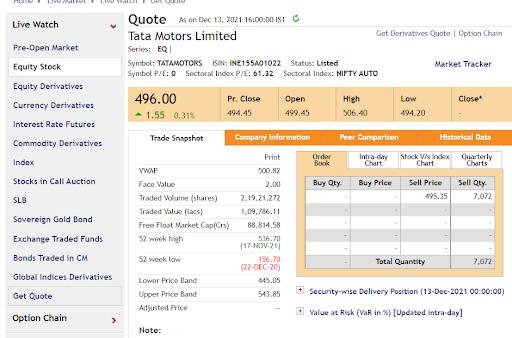

For example, the below is a snip of futures of Tata Motors shares, with different expiry dates. Let’s understand about expiry dates later, for now, our focus remains on understanding what I mean by a derivative.

Source: NSE India

Notice that the last column has details about the underlying value?

For a Tata Motors future, the underlying is obviously going to be a Tata Motors share. So, going by this logic, the share price of Tata Motors for today must be Rs.496, isn’t it?

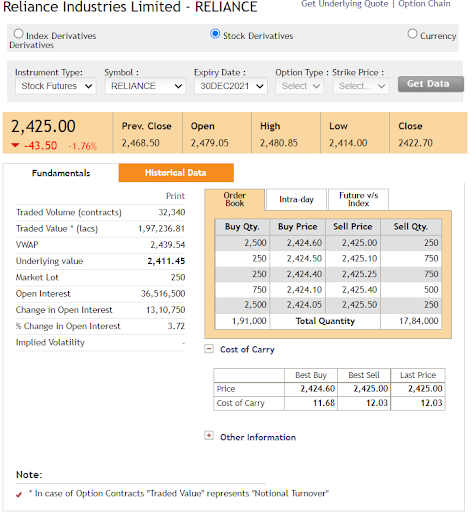

Well, here you go!

Source: NSE India

If we revisit our understanding of what is a derivative, which is a product whose value is derived from one or more underlying variables, we see that it seems to make more sense.

There are several types of derivative instruments in the market namely Forwards, Options, Futures, Swaps, Swaptions, Collars etc. Our present discussion is going to be limited to understanding what we mean by futures.

Understanding forward contracts.

A futures contract is a standardised form of what we call a forward contract. So, to understand a future better, let us first take a simple example to understand a forward contract. Now imagine a wheat farmer in Punjab. Let’s say that his harvest cycle is 6 months which means that if he sows in March, he can reap the wheat in September. In March, when the wheat costs Rs. 400 per kilo, he decides to begin his cropping mentally calculating his profits from this harvest. In September, once he has harvested his grains, he sets forth towards the mandi, mentally fantasising the good profits he is about to reap at Rs.400 a kilo. At the mandi though, owing to markets conditions, the price of wheat has fallen to Rs.350 a kilo, leading to a significant fall in the forecasted profits of the farmer.

In order to avoid this risk of fall in prices at a future date, what can the farmer possibly do while standing in March? If he has a mechanism to agree at a locked selling price of Rs.400/ kg with a promise of delivery at a later date, he would be able to lock his profits and hence mitigate his risk. Now, this is what we call a forward contract.

A forward contract is an agreement between two parties, where one party agrees to by an underlying instrument, be it stock, currency, index or a commodity at an agreed price on a future date from another party.

Transitioning from forwards to futures

Now, imagine about one lakh farmers wanting to do the same thing. All of them gather at a market, desperately seeking out potential buyers to agree upon prices for a future harvest. Apart from causing chaos, it could also have other repercussions like say, the risk of default on the part of the farmer or the buyer. To avoid all this, there enters a crucial player, the one called an Exchange. The exchange acts as an intermediary between the buyer and the seller to facilitate the trades, streamline quantities and delivery dates and so on. This standardisation of a forward trade through the system of exchange leads to the creation of a powerful derivative instrument called Futures. Also, another benefit of having an exchange as a middle man is that the burden of finding a counterparty is shifted onto them.

As with forward contracts, the agreement is completed on a future date, either by actual delivery of goods or by cash settlement of the difference between the current market price on the future date and the agreed price. In general, the futures market is used as an effective hedge tool to lock your price, however, in practice, there are several people who speculate through futures market as well.

Some of the common features of a futures trade that are worth understanding are as follows:

- The price of a future is correlated to the underlying.

- Futures contract sizes are standardised.

- Futures contracts are regulated by Exchanges.

- Futures contracts are time-bound.

- Futures trades are mostly cash-settled

How is profit or loss made on futures trade?

Now assume that you are buying one lot of Reliance futures December expiry at the current price of 2,425.

Let us assume that you are holding the contract until the expiry date i.e. 30th December. The value of your contract as on today will be Lot size multiplied by price today which is 250 * 2425 = Rs.6,06,250.

As on the expiry date, three possible scenarios enfold.

- The price moves to Rs.2,500

In this case, you are making a profit because your selling price which is Rs.2500 is more than your agreed price which is Rs.2,425. Thus, you are making a profit of Rs.75 per share. Your total profit which is 250 shares * Rs.75 per share = Rs.18,750 will be credited to your account.

- The price moves to Rs.2,400

You make a loss here. Your loss of Rs. 25 per share multiplied by 250 shares which equals Rs.6,250 will be debited from your account.

- The price remains at 2,425

In this case, your agreed price and the actual price is the same. You neither make a profit, nor a loss.

Note that you could either opt for a buy or a sell future. What this means is that you could either have an agreed price of Rs.2,425 per share at which you will buy the share on expiry or agreed selling price of Rs.2,425 upon expiry. Depending upon your assessment of how the market is going to unfold, you could choose your position.

A person who anticipates the market to fall would make a profit by selling futures now while a person who believes that the market would rise would make a profit by buying futures now.

Margins and Futures Profits or Loss

We saw above, theoretically, how one could profit from a futures trade. But in the practical world, with huge volume of players involved, how does the futures market operate? When the exchange acts as a regulator for huge volumes and several counterparties, what are the potential risks it faces?

What if all sellers chose not to honour the contract for a particular expiry? Since the NSE is the regulator, it has to compensate the buyers. But doing so would result in a huge loss for the NSE. Hence, to protect the financial risk of the contract and to prevent unnecessary speculation, the NSE often fixes a margin to be paid for each share or index to be traded in the futures segment. The calculation of margin is based on complicated algorithms, inherent volatility, value at risk and several other company-specific and market-specific factors. It is not a constant number and is subject to change. SEBI comes up with margin requirement modifications.

The initial margin percentage is a combination of what we call SPAN margin and exposure margin. The SPAN is a tool used to calculate the SPAN margin and it uses a portfolio-based approach. Exposure margin is usually charged in addition to the SPAN margin as an added security. The SPAN margin is usually needed to be maintained at all times failing which a penalty is charged while the exposure margin generally adjusts for any mark to market losses.

What is MTM?

MTM or Mark to Market is the mechanism by which profit in futures contracts are calculated.

Typically, in futures market, the profit or loss is calculated on a daily basis and reflected in your margin account.

Assume that you buy Reliance futures today at Rs.2,425 per share for a 250 lot size. Tomorrow, if the price rises to Rs. 2,450, a profit of Rs.25 per share or a total profit of Rs. 6,250 will be credited to your margin.

On the next day, if the futures price falls to Rs.2,400, the loss of Rs. (2,450-2,400) = Rs.50 per share or Rs. (12,500) is debited from your margin account.

Combining margin requirements and MTM

The below table shows you a snapshot of how your margin account appears like.

As you can see, the cash balance is nothing but your initial margin plus or minus your mark to market profit or loss. As long as your balance exceeds the SPAN margin, it is fine. On 16th, when your cash balance falls below your SPAN margin, your broker will do what is known as a Margin Call asking you to pump money into your margin account.

Futures Pricing

The next exciting thing to understand is the mechanism of futures pricing. Although much of technical trading doesn’t really require an understanding of this, advanced strategies might require one to understand this mechanism.

In the above example for Reliance Industries, we noticed that the current market price was Rs.2,411.25 whereas the futures price today was Rs. 2,425. This difference between the spot and the futures price is known as spread.

Futures Price = Spot Price * (1 + Risk free rate of interest * Days to expiry/365) – Dividends if any

Please note that the actual market future price may not equal the theoretical price calculated above due to demand-supply differences, any news, brokerage and other charges etc.

But in general, the actual futures price is very close to the theoretical futures price calculated.

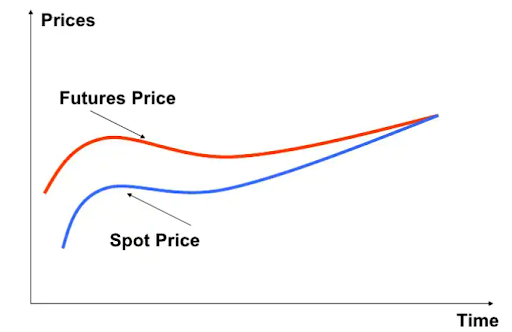

If the future price is higher than the spot, then the future is said to be trading at a premium or what is called Contango. Our Reliance example reflects this.

However, it is also possible for a future to be trading at below the spot price due to a negative outlook for the stock. Then the future is said to be trading at a discount or backwardation.

Upon expiry, the spot price and the futures price Converge since Reliance share and futures price on 31st December must essentially be the same.

Open Interest

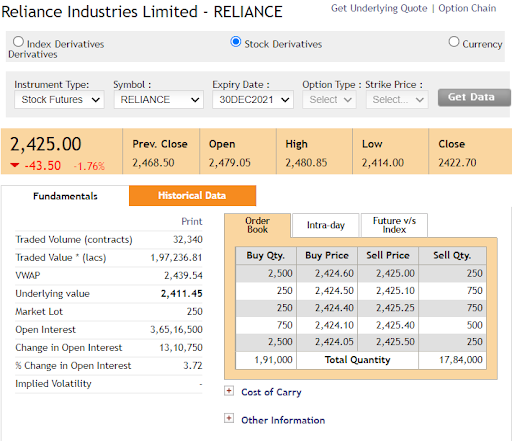

Another important measure, that is used frequently in derivatives trading is what is known as the open interest. In simple terms, Open Interest refers to the number of outstanding contracts open in the market for a particular expiry.

For instance, see the below snap shot.

In the above, we see Open Interest as 3,65,16,500. We also see a change in Open interest which is nothing but new contracts added or deleted to the particular scrip.

Conclusion

In summary, the future is an important derivative instrument used by hedgers and speculators for their respective requirements in the market.

- Its price is correlated to the underlying base

- It is cash-settled and traded in lots

- It gives you the benefit of leveraged trading

- It is regulated by Exchanges

Frequently Asked Questions

There are several risks associated with trading in futures. Some of them are.

- Leveraging - In futures contract, you get into a trade for a large number of shares with a little amount of money by paying a small fee called margin. For example, you can enter into a futures contract for Rs. 1,00,000 by depositing only Rs. 2,500. If you do not respect the margins and don’t settle then you will end in huge debts.

- Interest rate risk - SInce you are fixing the price of the future date today, there is a risk that on the given future date the rate of the commodity might be lower or higher which may or may not be in your favour.

- Liquidity risk - There is always a chance that there might not be another party to enter in the given price and hence it could be difficult to get out of a trade.

Future contracts are traded purely for profit. You can hold the futures contracts till the time the trade is closed before the expiry date. Today, with all regulations, it is closed on the third Friday of the month but it may vary depending on the contract so do check the specifications before entering into the trade.

If you hold on to future contracts till it expires then the clearinghouse will take it upon itself and matches the holder of a long contract against the holder of a short position. The holder of the long will have to place the entire value of the contract with the clearing house to take the delivery of the asset.

Margin money is a deposit paid to enter into a contract. It is taken as a safety measure to protect the interests of the seller and if the trade is done successfully then the margin money is returned back to the original account.