Understanding Share Buybacks: Meaning, How it Works, and Significance

May 25 2022 6 Min Read

A share buyback occurs when a company decides to purchase its own shares back from shareholders.

For a company, the cash used for the buyback lowers its assets, and the reduction in outstanding shares decreases equity.

This reduction in shares available in the market can increase the ownership stake of remaining investors and typically leads to a rise in earnings-per-share (EPS). This action may consequently lower the price-to-earnings (P/E) ratio, making the stock more attractive to potential investors.

After a buyback, the repurchased shares are either cancelled or held as treasury shares, meaning they are no longer considered publicly available or outstanding.

Share buybacks are executed to reduce the number of shares on the market, often leading to an increase in the share price due to the enhanced EPS. This can utilize excess cash effectively, consolidate ownership, or improve financial ratios and shareholder value.

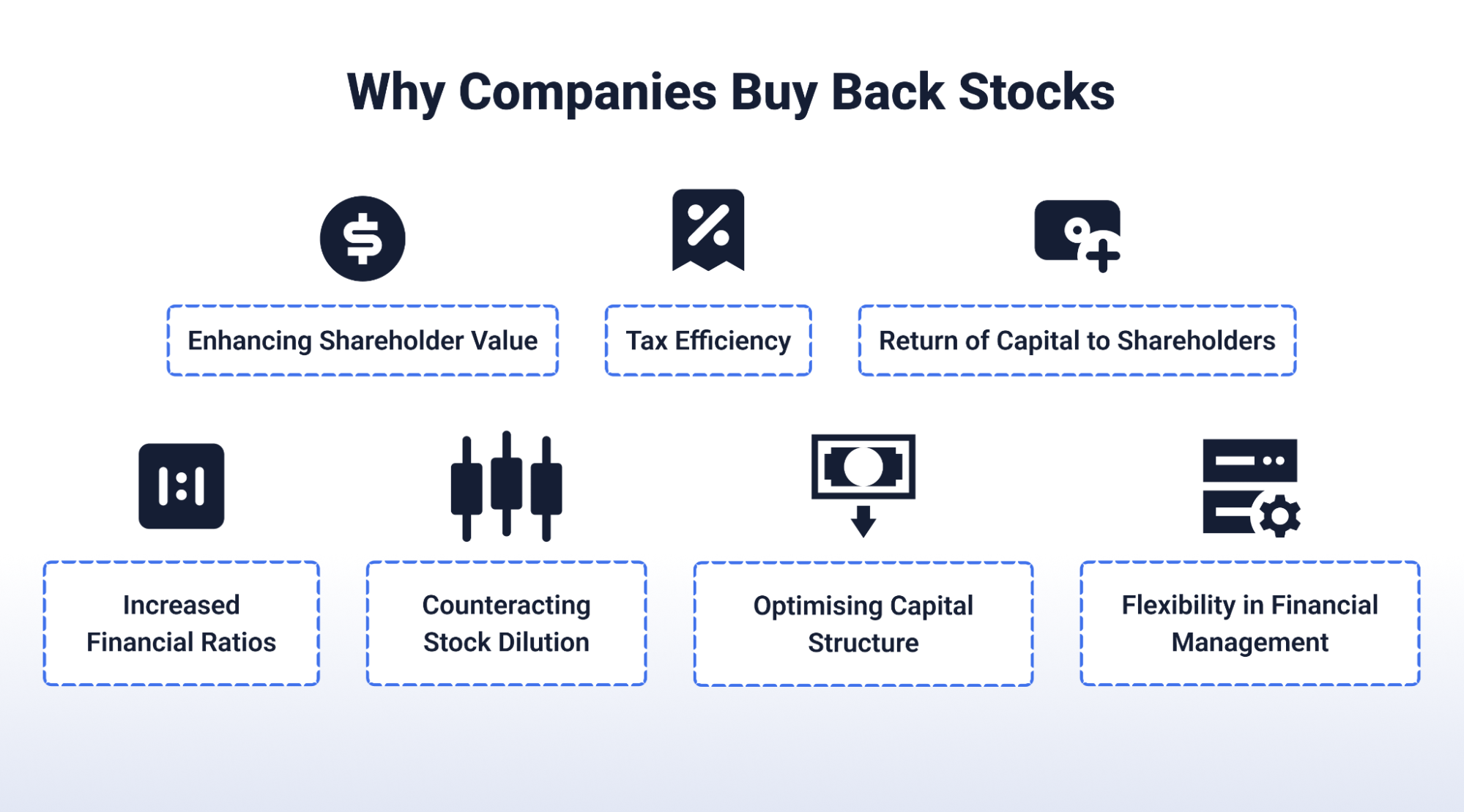

What Are the Reasons for Share Buyback?

Enhancing Shareholder Value

Companies often execute buybacks when they believe their stock is undervalued, using them as a tool to increase the stock price. This signals the management’s confidence in the company’s prospects in the market.

Tax Efficiency

Buybacks can be more tax-efficient compared to dividends since dividends are taxed at the dividend rate. On the other hand, the capital gains from the appreciated stocks due to buybacks are taxed at the capital gains rate, which is generally lower.

Increased Financial Ratios

Reducing the number of outstanding shares through buybacks often increases EPS and return on equity (ROE). This makes the company appear more profitable and financially stable.

Flexibility in Financial Management

Buybacks provide companies with the flexibility to return cash to shareholders without committing to ongoing payments, allowing for better cash flow management.

Counteracting Stock Dilution

Share buybacks are used to counteract the dilutive effects of stock options exercised by company employees and management, helping to stabilise or increase the stock price by reducing the overall share supply.

Return of Capital to Shareholders

Buybacks offer a way to return capital to shareholders that may provide a better yield on their investment, particularly when the company’s stock price is low.

Optimising Capital Structure

Companies may also use buybacks as a strategy to optimize their capital structure. Reducing equity can increase debt leverage, which might be more cost-effective if borrowing costs are lower compared to other returns.

What Is the Effect of Share Buyback?

The impact of a share buyback is complex. Primarily, it reduces the number of outstanding shares, potentially increasing the stock price and EPS, which can make the company appear more attractive to investors. This can also enhance the return on assets and equity. Buybacks often signal to the market that the company’s leadership believes the stock is undervalued, boosting investor confidence.

However, they can also reduce a company’s cash reserves, which might impact its ability to invest in growth opportunities or weather economic downturns. Overall, buybacks are used as a tool to manage financial perceptions and reward shareholders.

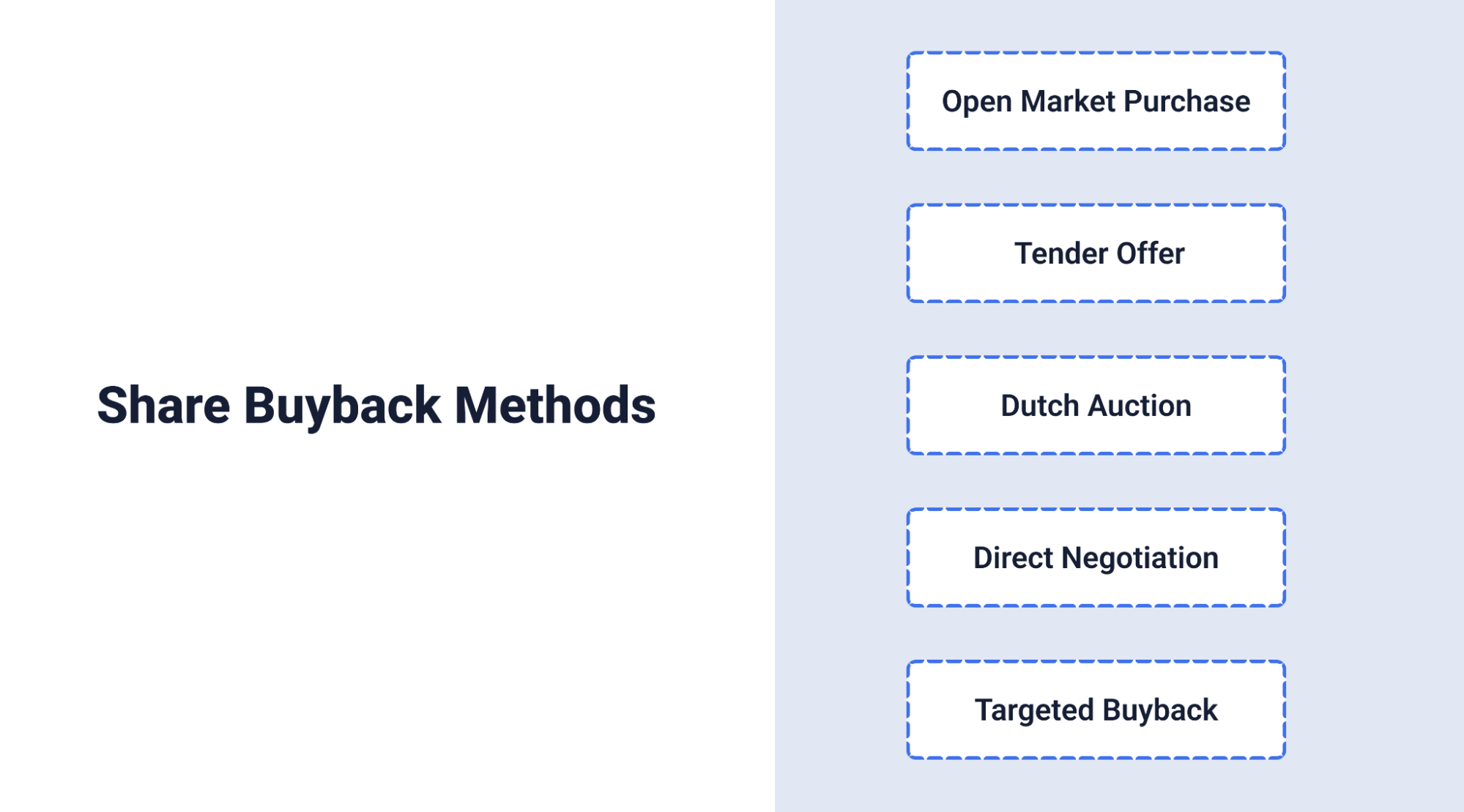

What Are the Different Methods of Share Buyback?

Share buybacks can be conducted through several methods, such as:

Open Market Purchases: This is the most frequent method where companies buy their shares directly from the open market over an extended period. This approach offers flexibility as the company can choose when and how many shares to buy, often based on the current stock price and market conditions.

Tender Offer: The company offers to purchase shares from shareholders at a premium to the current market price within a specific time frame. Shareholders can choose to sell all, part, or none of their shares back to the company. This method provides shareholders with a direct and immediate opportunity to exchange for cash.

Dutch Auction: The company announces a price range within which it is willing to buy back shares. Shareholders then indicate how many shares they wish to sell and at what price within this range. The company determines the buyback price after receiving all offers and buys back shares at this price from shareholders.

Direct Negotiation: The company purchases shares directly from a major shareholder or a group of shareholders, often at a negotiated price. This method is typically faster and can be tailored to specific large transactions.

Targeted Buyback: Companies may target specific blocks of shares for purchase, often from institutional investors, strategic partners, or former employees with large holdings. This is typically used to consolidate ownership or retire shares.

Each method has its advantages and potential drawbacks. The choice largely depends on the company’s objectives, the amount of money it intends to spend, and the market conditions.

What Is the Significance of Share Buyback to Investors?

The announcement of a share buyback often signals that a company anticipates future profitability, which can positively affect its stock price. Investors commonly interpret such announcements as indications of potential acquisitions, the launch of new products, or enhancements to existing product lines.

However, it’s important to note that companies may initiate buybacks not solely based on current profitability. Sometimes, the objective is to stabilise or enhance share value by reducing the surplus of available shares, thereby protecting the existing capital structure.

Therefore, while share buybacks can be a strong signal of confidence from company management, investors should consider a broader set of financial indicators before making investment decisions. Metrics such as market trends, earnings per share, and overall economic conditions are crucial for gaining a comprehensive understanding of the potential impact of a buyback on the company’s financial health.

What Are the Drawbacks of Share Buyback?

While share buybacks are often pursued to increase shareholder value, they have attracted criticism for various reasons, such as:

Inefficient Use of Capital: Share buybacks can sometimes represent a poor allocation of capital, especially when the funds could be used for more profitable ventures. Critics argue that these funds could instead be directed toward expansion, research, and development.

Increased Financial Risk: Particularly in volatile economic times, such as during a pandemic, companies might fund buybacks through debt. This approach can enhance earnings per share in the short run but increases the company’s financial risk.

Opportunity Cost: Allocating funds to buybacks might cause companies to miss out on other investment opportunities that could yield greater long-term benefits.

Short-term Focus: Executives, whose compensation often includes stock-based incentives, may prefer buybacks as they help lift the stock price, enhancing their earnings. This alignment of interests can lead to a short-term focus at the expense of long-term company health.

Weakened Shareholder Value: Buybacks may reduce the intrinsic value received by shareholders if the repurchased shares are overvalued. Additionally, if the repurchased stocks are used for compensating executives, it can dilute the value.

These concerns suggest that while buybacks can be an effective tool for managing shareholder value, they must be approached with a balanced perspective.

How Is Share Buyback Different From Dividends?

Share buybacks and dividends are both companies’ ways of benefiting the shareholders. However, they are entirely different in their fundamentals.

Here is a detailed comparison chart between dividends and share buybacks.

| Basis | Dividends | Share Buybacks |

| Meaning | Dividends are the profits earned by the company that are allocated, partly or wholly, to existing shareholders of the company. | A share buyback is the surrendering of a portion of shares by the surrendering shareholders to the company in return for a premium amount. |

| Effect on Share Count | The number of outstanding shares of the company remains the same. | The number of outstanding shares of the company decreases. |

| Occurrence | Typically distributed regularly (quarterly/annually). | Employed rarely under specific conditions. |

| Benefiting parties | Dividends benefit the existing shareholders. | Share buybacks benefit the selling shareholders. |

| Taxation | The dividends are taxed at 3 levels, with additional corporate taxes. | A dividend distribution tax of 20% is deducted from the earnings. For investors, it is taxed as capital gains. |

| Types | Dividends can be classified into regular, annual, special, or one-time dividends. | Share buybacks cannot be categorised into different genres. |

| Market Supply | No impact on the supply of shares in the market. | Reduces the supply of the number of outstanding shares of the company. |

| PE Ratio | Dividends show no direct effect on the PE Ratio. | Share buybacks tend to reduce the PE ratio. |

| Market Perception | Seen as a sign of financial health and consistency. | Viewed as a sign of stock being undervalued or adjustments in capital structure. |

| Net worth | Dividends do not contribute substantially to the net worth of the company. | Share buybacks are an excellent methodology for building the company’s net worth. |

Conclusion

Share buybacks play an important role in a company’s financial strategy, offering numerous benefits such as enhancing shareholder value, improving financial ratios, and signalling confidence in the company’s prospects. However, they also come with certain risks and must be managed carefully to avoid long-term financial pitfalls.

By understanding both the mechanics and implications of share buybacks, investors can better assess the health and strategic direction of a company.

As financial markets continue to evolve, staying informed about these practices will enable shareholders to make more educated decisions about their investments, aligning their financial goals with the actions of the companies they invest in.

Disclaimer: This article is for information purposes only and should not be considered as stock recommendation or advice to buy or sell shares of any company. Investing in the stock market can be risky. It is therefore advisable to research well or consult an investment advisor before investing in shares, derivatives or any other such financial instruments traded on the exchanges.

Frequently Asked Questions

No, you're not obligated to sell your shares back to the company during a buyback. It's entirely your choice whether to participate and sell your shares or retain them.

Share buybacks can be positive, signalling the company's confidence in its value or managing share dilution. However, the context and reasons behind the buyback greatly influence whether it's beneficial overall.

The procedure typically involves the company announcing the buyback, setting a price range, shareholders offering their shares, and the company then repurchasing a set amount based on the offers it receives.

Share prices may increase after a buyback due to the reduced number of shares in circulation, which can increase earnings per share and make the remaining shares more valuable. However, market conditions can also affect share price movement.

After a buyback, stocks often go up since the reduction in the number of available shares can lead to an increase in earnings per share and the perceived value of the remaining shares. However, this isn't a guaranteed outcome.