Welcome to the 13th edition of our Weekly Musings!

The high-frequency indicators such as rail freight, petrol and diesel, and power consumption suggest that the economic affairs of the country are only getting better. With an improvement in the Covid-19 situation (India has one the lowest case fatality ratio in the world) and a resulting uptick in economic activity, the consumption and output factors in the Q2 of FY21 weren’t as bad as anticipated.

Things started getting better when the two mobility indices, the Google Mobility Index (GMI), and the Apple Driving Index (ADI), showed a gradual recovery during the end of Q1 and Q2 of this financial year. While the GMI for groceries and pharmaceuticals improved to 80% of the pre-Covid levels by end of June 2020, the ADI, which was at 50% in June crossed the 80% mark by the end of September, thus matching the GMI levels.

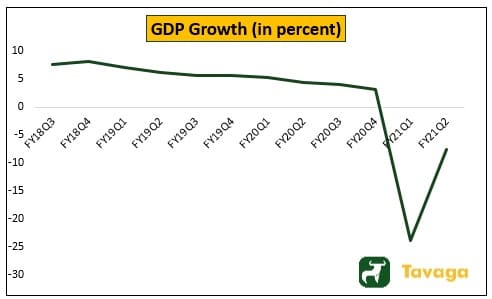

This development further leads to one more inference. The consumption activity only got better with the well to do iPhone users, who also propel the private consumption, showed readiness to move out and resort to discretionary spending. The Q1FY21 GDP contraction of 23.9 percent was on the expected lines due to the stringent lockdowns implemented across the nation. However, the recent GDP data published by the NSO points out a stellar rebound.

The idea here is not to directly correlate the improvement in mobility indices with economic growth, but consider it as a factor while gauging the consumption activity. If Q2 GDP figures brought cheers, it will be very early to infer the fact that the improvement in the trend would continue in the 3rd quarter as well. For the week ending 27th November, the GMI, which had reclaimed the pre-Covid levels during the festive seasons of Dussehra and Diwali, has again fallen back to 92 percent showing stagnation. Moreover, the ADI, which peaked in the second week of November, has fallen back to 75 percent.

Most of the bump in consumption in Q2 can be attributed to pent-up and festive demand. The continuity is of prime importance if the economy has to get stronger and resilient. Assuming that the rural and urban rich have further spurred private consumption, the opposite is the case with the urban poor. The pandemic has resulted in low household income, and the high inflation momentum in Q2 of this FY is expected to continue in the 3rd quarter as well due to various internal and external factors, thus ensuing consumption to be a low-key affair for the urban poor.

India bounces back from its lows; latest GDP figures show a solid rebound

India formally entered into the zone of technical recession after the NSO published the GDP growth figures for Q2FY21. Having contracted by 24 percent in the 1st quarter of FY21, the GDP growth in the 2nd quarter contracted at a slower pace of 7.5%.

The lockdown imposed by the state and central government had brought India to a grinding halt in the first quarter of this financial year, however, with the gradual opening of the economy in the second half of the calendar year 2020, the GDP growth moderated from 23.9 percent in the April-June quarter to 7.5 percent in the quarter ending September, beating all estimates, including that of RBI’s.

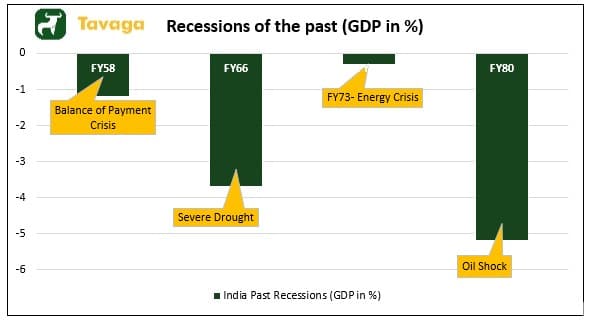

While this was the first-ever technical recession India faced, the country has witnessed 4 recessions in the past. Pre-1996 when rolling out the yearly GDP growth figures (and not every quarter) was a normal activity, India had contracted four times, thus leading to recessions.

Source: Tavaga Research

While the expenditure trends were well-in line with the expectations, the contraction in government final consumption expenditure came in as a shock as the expectation was such that the expenditure would spike due to various stimulus announcements.

|

Expenditure Trends |

Q3FY20 |

Q4FY20 |

Q1FY21 |

Q2FY21 |

| Private consumption | 6.6% | 2.7% | -26.7% | -11.3% |

| Investments | -5.2% | -6.5% | -47.1% | -7.3% |

| Government final consumption expenditure | 13.4% | 13.6% | 16.4% | -22.2% |

Source: Bloomberg Quint, Tavaga Research

As discussed above, several high-frequency indicators have sent strong signals of the economy moving into a positive trajectory soon, due to factors such as – festivities, pent-up demand, and India’s successful fight against the Covid-19 induced pandemic so far.

Along the expected lines, agriculture supported the real economy by registering a handsome growth of 3.4% yet again. However, the manufacturing sector made the news as the GVA (gross value added) clocked-in a growth of 0.6 percent against the much-anticipated contraction. While the healthy signs of a pick-up in manufacturing activity are encouraging, it is important to note that this rise was on a low base of negative growth of 0.6 percent in Q2FY20.

While a 7.5% contraction might uplift the spirits, the number would have been much better had the government continued its spending activity. With inflation on the rise, a rate cut from the central bank is ruled out for now, however, the accommodative stance of the RBI could end up in further softening of the yields.

Source: Tavaga Research

Core Sector contraction and Bank Credit growth to the industry remain signs of worry

On the back of a decline in production of crude oil, steel, natural gas, refinery products, the output of the eight core infrastructure sectors contracted by 2.5 percent in October 2020. From the eight core industries, fertilizers, coal, electricity, and cement registered positive growth. A contraction of 2.5 percent was much higher than September’s drop of 0.1 percent depicting a weak industrial recovery.

The core infrastructure sectors make up 40 percent of the IIP and the rest 60% is made by the non-core industries. The non-core sector is expected to continue with its outperformance over the core industries due to the pent-up demand, and hence the IIP could well remain in the positive trajectory for the short term.

The medium to the long-term outlook of IIP remains uncertain as the growth in the non-core sector is expected to stagnate and moderate once the pent-up demand effect satiates. Adding to the woes of industries, the banks’ credit growth to industries contracted by 1.7 percent in October at a time when the MSME sector is witnessing a robust credit growth.

Preliminary vaccine review of Pfizer and Moderna to shape the market movement in December

With the latest analysis showing the vaccine highly effective in preventing Covid-19, Moderna Inc requested an emergency use authorization subject to clearance from the U.S. FDA.

For the 196 cases treated upon at the start of the month, the shot was 94.1% effective as per the primary analysis. For the recent 30 severe cases treated upon, Moderna Inc indicated a 100% efficacy rate against the coronavirus after receiving a placebo.

The Pfizer-BioNTech shot was also submitted to the U.S FDA at the beginning of November and it will be reviewed before the Moderna shot gets reviewed. The last month of 2020 could show some signs of a bright 2021 if the preliminary vaccine review meetings, which are scheduled in the second and third week of December, end with a positive commentary.

Parts of the US continue to see a strong second wave of Covid-19 with daily cases soaring and hospitalizations rising. California, Texas, New Jersey, and New York could consider putting restrictions on commuters with a stay at home order.

Further, the recent commentary by Fed chief Jerome Powell points out more uncertainties despite the progress in the Covid-19 vaccine developments.

Retail traders and investors should stay cautiously optimistic on the vaccine news and avoid the use of leverage to take positions in the market, as it is difficult to say whether the vaccine shots developed by the two companies could get approved in the upcoming reviews.

Coming Up In The Week:

- Auto Sales Data – 1st November

- India Manufacturing PMI Data – 1st November

- RBI Policy Meet – 4th November

Happy Investing!

Download the Tavaga Mobile Application And Link Your Trade Smart Trading Account:

Trade Smart has tied up with Tavaga Advisory Services, a SEBI Registered Investment Adviser (RIA).

Through the Trade Smart-Tavaga partnership, both companies intend to democratize investment advisory and cater to investors’ goals and needs through more transparent and efficient investing.

Tavaga & Trade Smart has issued this report for information purposes only. This is not an investment document. Please refer to https://tavaga.com/terms.html for disclaimers.