Let’s Meet Delta !

Get to know more about delta & its reciprocity with online trading

In the world of Options, one of the most commonly known and widely used terminology is ‘Delta’. It is essentially a risk measure that represents the sensitivity of an option’s price to the underlying asset.

Delta can be defined as the rate of change in the option’s price as a result of a change in the price of the underlying asset. This particular Greek provides an invaluable insight to the option traders regarding the expected movement in price of an option given any changes in price of underlying asset.

In Stock Market, Delta value ranges between 0 and 1 for a call option and -1 to 0 for put option. This would imply that for a given increase in the price of underlying asset, the price of a call option would also increase where the price of a put option would move inversely.

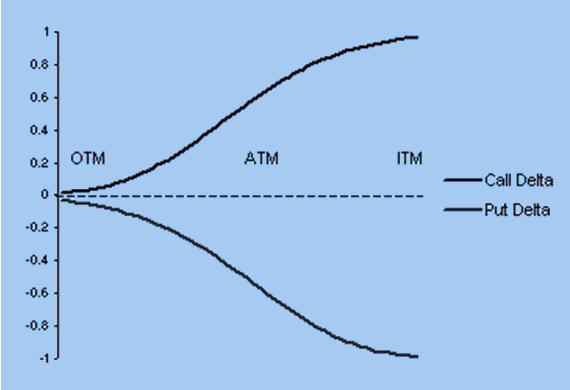

An important factor which determines the ‘value’ of Delta for a Call/Put option is its ‘Moneyness’, as depicted in the below figure.

| Call Option | Put Option | |

| In the Money | 0.5<Delta<1.0 | -1<Delta<-0.5 |

| At the Money | 0.5 | -0.5 |

| Out of Money | 0<Delta<0.5 | -0.5<Delta<0 |

An ‘At the money’ Call or Put option is likely to have a Delta value close to 0.5. For both Call & Put options, a Far ‘Out of the money’ option will have a delta close to zero whereas Deep ‘In the money option’ will have large delta values.

In order to effectively utilize Delta for buying and online trading of options in stock market, it is really important to understand the factors which can cause Delta value of an option to change. The Delta of an option can vary due to any of these 3 factors – a) a change in the underlying asset’s price, b) change in implied volatility of the option and c) Passage of time or the time of expiration for an option contract. The first factor here is captured by Gamma which measures how much Delta changes with respect to change in price of underlying asset.

The reason behind the immense popularity of online trading in Delta among Option traders is due to its usefulness as a Hedge Ratio. In order to offset the risk related to changes in price of the underlying asset, option investors enter into long or short positions in the underlying stock. For example, an investor with a long call position can hedge by shorting the underlying stock. The delta value gives us how much of the long or short position of the underlying asset needs to be purchased. If you hold a portfolio with a number of option positions, the Delta for the entire portfolio can be calculated by adding up the deltas of individual option positions. The point to note here is that for short Call & short Put positions, the delta signs get reversed. This additive property of Delta further makes it a highly effective portfolio management tool.

| Long Call | Short Call | Long Put | Short Put | |

| Position Delta | Positive | Negative | Negative | Positive |

Start Online Trading

In Stock Market Now

[email-subscribers namefield=”NO” desc=”Subscribe now to get latest updates!” group=”Public”]

Thanks for the comment Ravi. Glad, you like our services. We aim at improving it everytime and continue delighting our customers with the best services at the lowest costs.

I have a account in sharekhan brokerage is very high and hidden costs , sharekhan make foolish and cheat to customers, but trade smart is very hood for traders , investors and others very low brokerage, I search online trade smart is good I talk to customer care Naveli mam clear my all confusion thanks a lot to smart trade